Days payable outstanding (DPO) is defined as the average number of days a business takes to pay its supplier invoices, making it one of the most direct measures of working capital management available to finance professionals. A higher DPO means your business holds cash longer before paying suppliers. That retained cash can fund operations, cover payroll, or reduce short-term borrowing costs. For Canadian business owners managing tight liquidity cycles, understanding and controlling DPO is not optional. It is a core discipline of financial health.

What is days payable outstanding and how does it work?

Days payable outstanding measures how efficiently a business manages its accounts payable cycle. The metric sits at the intersection of cash flow strategy and supplier relationship management. A business with a DPO of 45 days pays its suppliers, on average, 45 days after receiving an invoice. That 45-day window represents free working capital the business can deploy elsewhere.

DPO is also a signal to lenders and investors. A very low DPO suggests a business pays suppliers faster than necessary, effectively giving suppliers an interest-free loan. A very high DPO can signal cash flow stress or strained supplier relationships. The goal is a DPO that reflects deliberate payment timing, not accidental or reactive behavior.

Procurement teams directly influence DPO through the payment terms they negotiate. Net-30, Net-60, and Net-90 terms set the ceiling for how long a business can legally hold payment. Finance teams then determine whether the business actually uses that full window. Most businesses do not, which is a significant-missed opportunity.

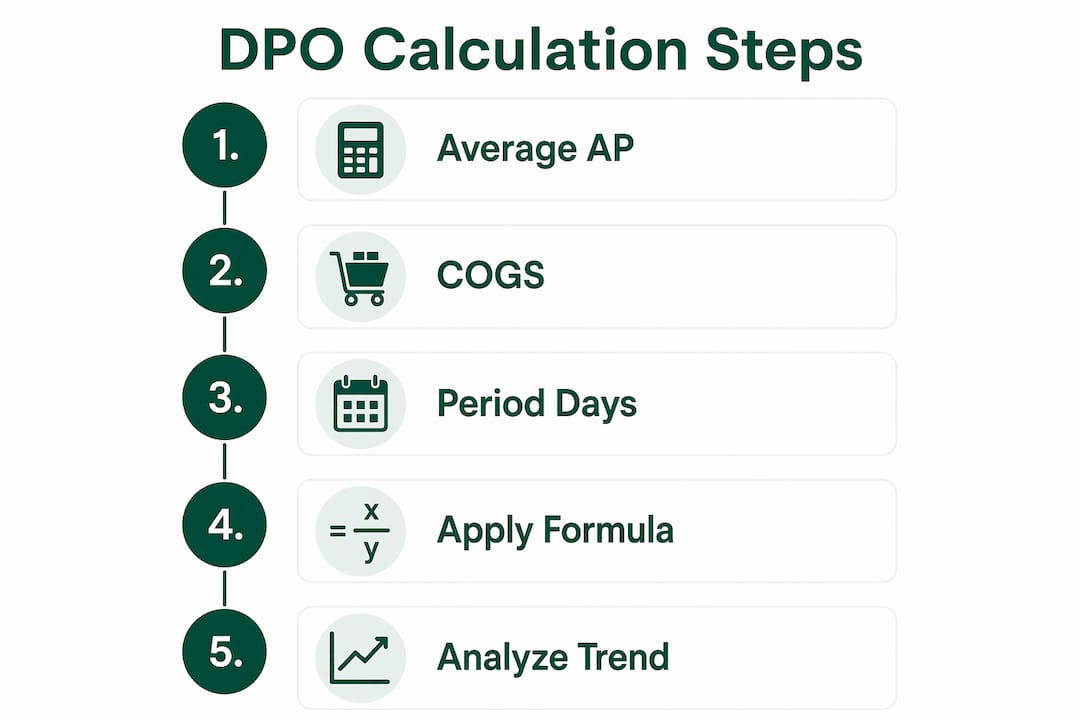

How to calculate days payable outstanding with accuracy

The standard DPO formula is straightforward: (Average Accounts Payable / Cost of Goods Sold) × Number of Days in Period. Use 365 days for an annual calculation and 90 days for a quarterly one. This formula gives you a reliable picture of your payment cycle when applied consistently.

Choosing the right accounts payable figure

Average accounts payable produces more accurate results than a single end-of-period snapshot. Calculate it as (Beginning AP + Ending AP) / 2. A snapshot taken at month-end can be misleading if your business pays a large batch of invoices just before the period closes. The average smooths out that distortion.

Adapting the calculation for different periods

| Period | Days Used | AP Figure |

|---|---|---|

| Annual | 365 | Average of Jan 1 and Dec 31 AP |

| Quarterly | 90 | Average of quarter start and end AP |

| Monthly | 30 | Average of month start and end AP |

Quarterly DPO calculations work well for businesses with seasonal revenue swings. Seasonal fluctuations in COGS affect DPO calculations directly. High-revenue periods increase the COGS denominator, which artificially lowers DPO if you rely on single-period snapshots. Rolling averages correct for this and give you a more accurate trend line.

Pro Tip: Run your DPO calculation monthly and track it as a trend, not a single data point. A DPO that drops three months in a row tells you more than any single number.

A practical example

Assume your business ends the year with $180,000 in accounts payable, started with $120,000, and recorded $1,200,000 in COGS. Average AP is $150,000. The DPO calculation is ($150,000 / $1,200,000) × 365 = 45.6 days. That result tells you the business takes roughly 46 days on average to pay suppliers.

What is a good DPO? Industry benchmarks explained

Median DPO across industries sits at approximately 38 days as of 2025. That median masks wide variation by sector, company size, and supplier terms. A DPO of 38 days is healthy for a retailer and dangerously low for a manufacturer with 90-day terms available.

| Industry | Typical DPO Range |

|---|---|

| Manufacturing | 45–90 days |

| Technology | 30–60 days |

| Retail | 20–45 days |

| Food service | 15–30 days |

These ranges reflect negotiated norms within each sector. Manufacturing businesses carry large raw material purchases and typically negotiate longer terms. Retail businesses turn inventory quickly and often face supplier pressure for faster payment. Food service operates on the tightest margins and shortest payment windows of any major sector.

Several factors shift where your business falls within these ranges:

- Company size. Larger businesses command better terms because suppliers value the volume.

- Supplier concentration. If one supplier represents 40% of your purchases, that supplier holds negotiating power.

- Payment history. A track record of on-time payment gives you credibility to request extended terms.

- Industry norms. Suppliers calibrate their terms to what competitors accept.

Never interpret DPO in isolation. A DPO of 60 days looks strong for a manufacturer and alarming for a food distributor. Compare your DPO against your own trend line first, then against sector benchmarks. A DPO rising without a corresponding improvement in cash flow often signals a problem, not a win.

How to improve DPO without damaging supplier relationships

Optimizing DPO means aligning payment timing with your cash management goals, not simply delaying every invoice as long as possible. The distinction matters. Arbitrary delays damage supplier trust. Deliberate, terms-aligned payment timing builds it.

"Most companies pay earlier than their payment terms require, which reduces potential liquidity benefits. Paying on the due date maximizes your credit float. Paying early is effectively an interest-free loan to your suppliers."

The five most effective methods to improve DPO are:

- Negotiate extended payment terms. Request Net-60 or Net-90 terms from key suppliers, especially if you have strong payment history or high purchase volume. Frame the conversation around partnership, not pressure.

- Implement accounts payable automation. AP automation provides real-time visibility into invoice status, preventing premature payments and enabling proactive management without risking supplier relationships.

- Schedule payments to the due date. Set payment runs to release funds on the due date, not before. This single discipline can add 5–10 days to your DPO without any renegotiation.

- Review DPO monthly by supplier and category. Aggregate DPO hides the detail you need. Tracking DPO by supplier reveals where you are paying early unnecessarily and where you may be approaching late payment risk.

- Monitor early payment discount offers carefully. A 2% discount for payment within 10 days (2/10 Net-30) equates to an annualized return of roughly 36%. Accept those discounts selectively when cash allows. Reject them when liquidity is tight.

Pro Tip: Build a supplier payment calendar that maps each vendor's due date against your cash flow forecast. This prevents both early payments and accidental late ones.

Excessively high DPO carries real risks. Suppliers may tighten terms, reduce credit limits, or deprioritize your orders during supply crunches. The goal is a DPO that sits at the upper edge of your negotiated terms, not beyond them.

How does DPO fit into the cash conversion cycle?

The cash conversion cycle (CCC) measures how long it takes a business to convert its investments in inventory and other resources into cash from sales. The CCC formula is: CCC = Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) – DPO. A lower CCC means faster cash recovery.

DPO is the only component of the CCC that reduces the cycle when it increases. Every additional day you extend payables is one less day your cash is tied up. That is why DPO improvement has a direct, measurable impact on working capital efficiency.

| CCC Component | What it measures | Impact on CCC |

|---|---|---|

| DSO | Days to collect from customers | Higher DSO increases CCC |

| DIO | Days inventory sits before selling | Higher DIO increases CCC |

| DPO | Days to pay suppliers | Higher DPO decreases CCC |

The practical implication is clear. Improving DPO alone does not guarantee a better CCC if DSO and DIO are rising at the same time. A business that extends payables to 60 days but also lets receivables slip to 75 days has not improved its working capital position. It has shifted the problem.

The most effective approach balances all three metrics:

- Reduce DSO by tightening customer credit terms and accelerating collections.

- Reduce DIO by improving inventory forecasting and reducing safety stock where possible.

- Increase DPO by negotiating better terms and enforcing payment discipline.

Focusing on DPO in isolation is a common mistake. Finance professionals who track all three metrics together get a complete picture of where cash is being consumed and where it can be freed.

Key Takeaways

Managing days payable outstanding effectively requires deliberate payment timing, supplier-level tracking, and integration with the full cash conversion cycle.

| Point | Details |

|---|---|

| Use the correct DPO formula | Apply (Average AP / COGS) × days in period; use rolling averages to correct for seasonal distortion. |

| Benchmark against your sector | Median DPO is approximately 38 days, but manufacturing typically runs 45–90 days and retail 20–45 days. |

| Pay on the due date, not before | Paying early is an interest-free loan to suppliers; scheduling to the due date maximizes your cash float. |

| Track DPO by supplier, not just in aggregate | Aggregate DPO hides early payments to low-priority vendors and late payments to critical ones. |

| Integrate DPO with DSO and DIO | Improving DPO only improves working capital if DSO and DIO are also managed actively. |

DPO as a financial lever, not just a metric

At Monimate, we have seen a consistent pattern among businesses that struggle with cash flow. They track DPO as a reporting exercise rather than a management tool. The number gets calculated, filed in a monthly report, and rarely acted on. That approach leaves real money on the table.

The insight that changed how we think about DPO came from watching businesses track it at the aggregate level only. A company might report a healthy average DPO of 50 days while simultaneously paying its three most critical suppliers in 15 days and stretching a lower-priority vendor to 90 days. The average looks fine. The underlying behavior is chaotic.

Supplier-specific DPO tracking is where the real work happens. When you know exactly how many days you are taking to pay each vendor against their contracted terms, you can make deliberate decisions. You can prioritize payment to suppliers who offer early payment discounts worth taking. You can hold payment to the due date for suppliers where no discount applies. That level of control does not come from a monthly aggregate report.

Seasonal distortion is the other issue most finance teams underestimate. A Canadian retailer running DPO calculations through the fourth quarter will see COGS spike, which compresses the DPO figure even if payment behavior has not changed. Rolling 12-month averages correct for this. Single-period snapshots do not.

The businesses that use DPO most effectively treat it as a cash flow lever they adjust deliberately, not a number they observe passively.

— Monimate

How Monimate supports your accounts payable strategy

Managing DPO well requires visibility you cannot get from a spreadsheet updated once a month.

Monimate gives business owners and finance professionals real-time cash flow monitoring and predictive alerts that flag upcoming payment obligations before they create pressure. The platform's forecasting tools show you exactly when supplier payments will hit your account, so you can schedule them to the due date with confidence rather than paying early out of caution. For Canadian businesses managing multiple supplier relationships, Monimate's cash flow insights connect payment timing directly to liquidity forecasts, giving you the data to negotiate better terms and hold them without risking supplier relationships. You can also explore Monimate's financial ratio guides to build deeper fluency in working capital metrics like DPO, DSO, and the full cash conversion cycle.

FAQ

What is the standard DPO formula?

The standard formula is (Average Accounts Payable / Cost of Goods Sold) × Number of Days in Period. Use 365 for annual calculations and 90 for quarterly ones.

What is a good days payable outstanding ratio?

A good DPO depends on your industry. The cross-industry median sits at approximately 38 days, but manufacturing businesses typically target 45–90 days and retailers 20–45 days.

How does improving DPO affect cash flow?

A higher DPO means your business holds cash longer before paying suppliers. That retained cash reduces the need for short-term borrowing and improves working capital availability.

Can a DPO be too high?

Yes. A DPO that exceeds your negotiated payment terms signals late payment, which can damage supplier relationships, trigger tighter credit limits, and reduce your priority during supply shortages.

How does DPO relate to the cash conversion cycle?

DPO is subtracted from the cash conversion cycle formula (CCC = DSO + DIO – DPO). Increasing DPO directly reduces the CCC, which means your business recovers cash from operations faster.